Money can feel complicated and overwhelming. Between keeping track of payment dates, when the next paycheck hits, all the checking, savings, and credit cards accounts, retirement investments, and savings goals, there can be a lot of moving parts. And to top it all off, we are human; we are guaranteed to make a mistake eventually: missing a credit card payment, overdrafting the checking account, or neglecting to save and invest for our future. All this complication leads to having to make constant money-management decisions, adding another chore and stressor to life.

It doesn’t have to be this way. With some front-loaded effort, you can make your money do exactly what you need it to do without a second thought. How does a life without worrying about the timing of your next paycheck sound?

What you need (and what I’ve developed) are a Flow for your money to follow and an automated, organized system to execute it. When properly implemented together, you’ve achieved what I call “Automatic Money.” If you do the work in the beginning to set this up, you’ll rarely have to think about when and where your money is ever again—it will be where it needs to be before you can even think to check it.

Below, I’ll go into detail regarding Part I of Automatic Money: The 5 Stage Flow. In the following issue of The Trident, I’ll discuss Part II: The Structure.

Part I: The 5 Stage Flow

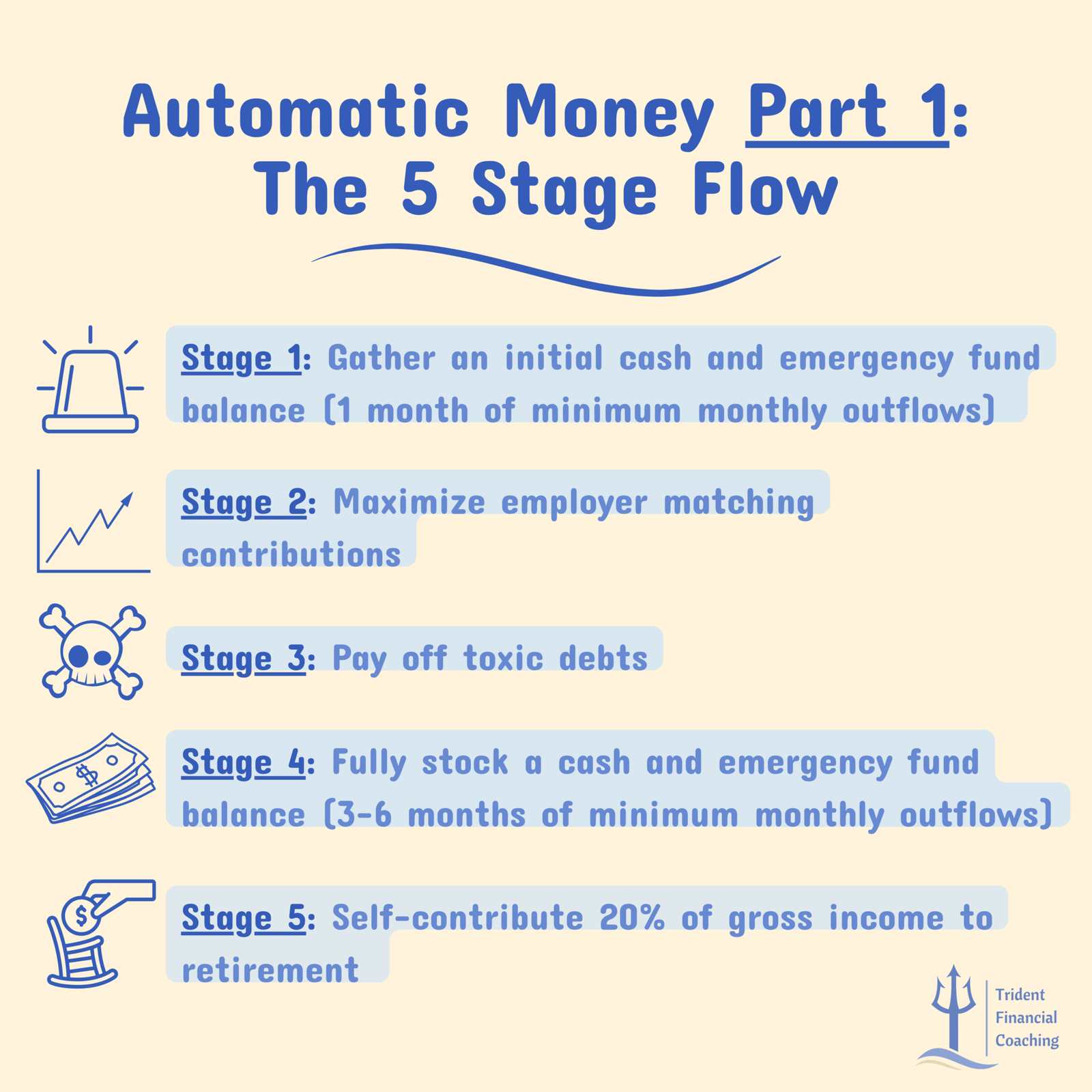

Achieving Automatic Money starts with you knowing what you should be doing with the next dollar that you have to work with. That’s where the “5 Stage Flow” comes in: 5 Stages that tell you where your next dollar should go to have it do the maximum work for you.

While each of the Stages could (and probably will) have their own dedicated The Trident blog post to get into the details, a brief description to give you an understanding will have to suffice for now. Here are the Stages:

Stage 1: Gather an initial cash and emergency fund balance

The first thing you need to do with your money is set a financial foundation by gathering a small pile of cash to buffer you from the happenings of everyday life. Doing this is pretty simple:

- Figure out your minimum monthly outflows (how much would you need to spend in a month if you cut your life down to the bare essentials?)

- Save up that number in cash and organize it:

- Half should sit in your high-yield savings account as an initial emergency fund

- Half should sit in your primary checking account as an "operating cushion" against overdrafting if you have an unexpected and/or larger-than-average bill

Stage 2: Maximize employer matching contributions

Once your initial cash and emergency funds are set aside, the next best way to deploy your money is to get every possible dollar from your employer in terms of contribution matching. Whatever the retirement-related account is (401(k), 403(b), 457(b), HSA, pension, etc.), make sure you’re getting every dollar your employer is willing to give you. As a percentage, this is going to be a higher return on your money than even most high interest debts. Consider making these contributions traditional rather than Roth to help with cash flow, especially if your focus is the following:

Stage 3: Pay off toxic debts

The next best return that you’re going to get on your money is paying off toxic debts. More specifically, pay off debts with high interest rates and/or that aren’t “productive.” These debts include, but are not limited to:

- Credit cards

- Personal loans

- Most car loans

- 401(k) loans

- HELOCs

- Student Loans with high interest rates (4-5% or higher)

The order in which you pay these debts down depends on your strengths and weaknesses regarding your behavior and mindset with money. There are two popular methodologies:

- The Snowball method, in which you pay down debts by putting your money towards the smallest debt (while still making minimum payments on everything)

- This method attempts to award you and get you motivated by catching some quick pay-offs as you clear the small debts

- The Avalanche method, in which you pay down debts by putting your money towards the debt with the highest interest rate (while still making minimum payments on everything)

- This method is the most efficient way to pay off debt by saving on interest, but some may find it difficult to continue if they feel they aren't "making progress" by fully eliminating some debts

Each method has its pros and cons, and everyone will need to decide for themselves which method works best for their specific set of circumstances.

Stage 4: Fully stock a cash and emergency fund balance

After toxic debts have been taken care of, it’s time to add more to the small pile of cash you built up back in Stage 1. Aim to pull together at least 3 months worth of your minimum monthly outflows and split it up accordingly:

- 2 months should sit in your high-yield savings account as a minimum fully stocked emergency fund

- 1 month should sit in your primary checking account, still as an "operating cushion"

To de-risk further, you can extend your emergency fund to hold up to 6 months of minimum monthly outflows. Completing this Stage should provide a sturdy financial foundation, ensuring your “now” and “near future” are taken care of.

Stage 5: Self-contribute 20% of gross income to retirement

Now you can begin to aggressively address your financial future by self-contributing at least 20% of your gross income to retirement accounts. Exclude employer matching contributions from this 20% calculation (hence “self-contributing”). Proceed in the following order:

- Max out an IRA

- For most, this will be a Roth IRA. Look up the income contribution limits for a Roth IRA to make sure you're eligible

- If you aren't eligible, a Traditional IRA is just as good (or a back-door Roth)

- Max out a HSA

- You may have already started this process in Stage 2 if your employer offers a HSA match

- Depending on your specific situation and goals, do either or both of the following until you've reached the "self-contributing 20% of gross income" threshold:

- Go back to your employer-sponsored retirement plan (401(k), 403(b), 457(b), pension, etc.)

- Contribute to a taxable brokerage account

Your Money Post-Flow

Once you’ve made it through the 5 Stage Flow, you have the ability to fully decide how you want to use the rest of your money. Whether the excess goes to saving more for different goals (vacations, education, a home, a car), spending more on lifestyle and hobbies, or charitable giving, you have the freedom to make those choices because you’ve taken care of all necessary business up to that point.

However, keep this in mind: there is no one-size-fits-all when it comes to personal finance. Depending on your specific financial situation, you may find some of the Stages feel unobtainable; others may feel that the Stages don’t account for enough. You need to have an understanding of the unique factors that shape your financial life and mold the 5 Stage Flow accordingly.

At the end of the day, achieving Automatic Money is the goal: we want our money to be where it needs to be before we can even think to check it. The 5 Stage Flow is the foundation for this, but there is more that needs to be done.

Check out the next issue of The Trident called “Automatic Money—Part II: The Structure” to learn more about achieving Automatic Money!

"Is Financial Coaching Right for You?" Questionnaire

Fill out this questionnaire to gauge your understanding of your finances and see if Trident Financial Coaching could benefit you!

Schedule a Free Consultation

Schedule your free consultation here and receive a discount code for a future booking!

Check out the Free Resources!

I've developed various calculators and tools for you to use to help get your financial life in order. Check them out!